Innovation Day brought together COOs, Heads of Operations and other industry leaders for a day of insight, discussion and connection in London.

Attendees and expert speakers explored the hottest topics in Operations across roundtables, plenaries and panel sessions. We’ve collected some of the best and sharpest insights below. Read on for a comprehensive review, or use the links to jump to your favourite topic.

- Innovation group sessions

- Tackling tomorrow’s challenges

- Oliver Wyman 2025 industry outlook

- AI: The road to productivity?

- The COO’s perspective: Building blocks for transformation success

- Future of Ops: Building the next-gen operating model

- Key takeaways from Innovation Day

Innovation group sessions

Dele Yussuf, Solutions Consultant at Duco, presents to Innovation Group attendees

Our morning sessions had one key aim: to shape the future of data automation.

Select Duco clients joined our Product team to discuss and refine the vision for our platform. We leveraged the time to tackle some of the biggest challenges in Operations.

These included issues such as the amount of manual work involved in dealing with non-standardised data and high volumes of exceptions.

Lack of transparency over data quality trends and reconciliation readiness was another hot topic, along with the issue of integration. How could firms improve integration, not just between systems but between Ops professionals with different roles, such as reconciliation builders and operators?

Clients also had the opportunity to share their ideas directly with our Product team. These included new features and capabilities that would give them even more ways to unlock efficiency, transparency and agility.

Tackling tomorrow’s challenges: Innovation at Duco

Duco Chief Product Officer James Maxfield on stage

Our Chief Product Officer, James Maxfield, took to the stage to share the outlook for innovation, both at Duco and across the industry. He had five key observations, based on conversations with industry leaders, about what the latter half of the decade has in store:

- On-prem is dead – or will be soon. No one wants to be the last one reliant on an on-premise system when everything else is in the cloud. Leaders won’t want to spend seven figures on an upgrade or retesting a system, either.

- Collaboration is key. Firms need to work together to solve their challenges. For instance, by getting different vendors to join forces against common challenges.

- Hyper automation is nearly here. The practice is gaining momentum. Things like the European move to T+1 in 2027 will put more pressure on outdated ways of working such as overnight batch processes.

- Employee experience is key. James shared how one client told us that Duco is helping to build the workforce of the future by letting talent “own their destiny”.

- Experience counts for vendors. It’s important that firms pick their partners carefully, do their due diligence and speak to other customers.

It was interesting, then, to see that legacy systems were the second-most common blocker for our audience in terms of achieving their 2025 goals. These systems are usually on-premise, so the coming five years could see a mass migration away from this kind of technology.

The poll also flagged manual processes as a big blocker – something that significantly worsens the employee experience. They are also usually symptomatic of automation gaps, which makes realising the potential of hyperautomation impossible as well.

But data quality was the top challenge, chosen by 51% of our audience. Ensuring that data is accurate, valid, complete, and consistent is clearly still a big issue for firms in the current environment.

James shared some of the ways Duco plans to help firms tackle these big challenges with a sneak peek at our roadmap. He also recapped the innovation we’ve delivered over the past year, including the acquisition of Metamaze and launch of Duco adaptive intelligent document processing (AIDP).

Oliver Wyman: Key industry trends for 2025

Christopher Rigby (Oliver Wyman)

Next up was Oliver Wyman partner Christopher Rigby, who was there to present the latest joint research by Oliver Wyman and Morgan Stanley on the industry trends and outlook for 2025.

Things got off to a great start when Christopher shared that, unlike last year, the industry outlook for the year is positive. Revenues hit $584bn in 2024, up 7% on 2023 and considerably higher than the long-run historical average of $520bn.

These higher revenues are here to stay: return on equity is expected to be 15% in 2025, which is materially above the cost of capital.

So what does this mean for firms? Investors are both expecting firms to have money to spare, and that they spend it wisely. Investors want to see firms tackling those long-term structural issues that drive inefficiency, such as data quality and legacy technology.

Christopher then identified some of the top priorities for COOs, based on conversations with industry leaders:

- Unlocking efficiency and increasing productivity

- Building scalable platforms

- Ensuring strong return on investment in technology

- Leveraging data to get full value from it

- Rethinking the traditional siloed approach; bringing Run-the-Bank and Change-the-Bank teams together

Banks have a lot to look forward to in the coming year. They’ll have the opportunity to fix some expensive long-standing challenges that have held them back for years. But along with that opportunity comes an expectation from the market that this is what they will do. It’s time for banks to deliver.

AI: The road to productivity?

Left to right: Christian Nentwich (Duco), Silvia Prieto (AWS), Arif Khan (Writer), Theresa Bercich (Lucinity) and Richard Mabey (Juro)

Our first panel of the day saw Duco founder Christian Nentwich moderating a discussion on how to successfully deliver AI tools in production. The panellists were:

- Silvia Prieto, Head of GenAI and ML for Financial Services at AWS

- Arif Khan, Strategic CSM for EMEA and APJ at Writer

- Theresa Bercich, Co-founder and CPO at Lucinity

- Richard Mabey, Co-founder and CEO of Juro

Christian began by outlining the state of enterprise AI: 80% of all projects fail – double the rate of IT projects in general. So what makes a successful project? Christian asked our panellists what they have live in production for customers.

The answers all had something in common: they were specific use cases with a narrowly-defined scope where it was easy to prove the value being delivered. For instance:

- Automatically marking up legal contracts

- Performing negative news searches for financial crime investigations

- Creating a draft portfolio proposal for wealth managers

- Or researching ultra-high net worth individuals to enable relationship managers to quickly personalise their pitches

Some of these tools work in the background, while others require the user to interact with them. What should the user experience be?

The panel said this is an important topic that is often overlooked. For example, if a user has 20 different AI co-pilot tools on their desktop, how are they going to cope with that? There’s a difference between screen estate and mental estate.

Part of the key to solving this is to understand what kind of AI is needed for any particular task. Some use cases require the user to interact with the AI directly, such as looking at a graph database to investigate very complex money flows. Other times, AI should just work in the background – generating the aforementioned graph, for example.

The panel ended with a discussion about agents. These are AI tools that can emulate human behaviour; learn from feedback, understand goals and plan how to achieve them, and take actions. For example, a document processing agent could look up reference data in an external system, add new data to systems, or send an email request for more information.

The panel all agreed that agents are the future, although it depends on the use case and what you trust the machine to do.

The COO’s perspective: Building blocks for transformation success

Left to right: Mia Kershaw (PwC), Jodie Kelsall (Britannia) and Cressida Hamilton (Chryse Coaching)

For our next panel, James Maxfield welcomed experts with three different perspectives on delivering, managing or helping to deliver transformational change:

- Jodie Kelsall, COO at Britannia Global Markets

- Mia Kershaw, Financial Services Operations Consultant at PwC UK

- Cressida Hamilton, Founder and CEO at Chryse Coaching

Mia kicked things off with a presentation of the findings from the latest report published by PwC and the Association of Financial Markets Europe (AFME) on the industry trends and challenges as perceived by COOs. Key priorities for transformation initiatives included:

- Prioritising cost efficiency

- Creating hybrid operating models

- Enhancing data-driven operations

- Leveraging cloud technology and AI

- The evolving role of operations leaders

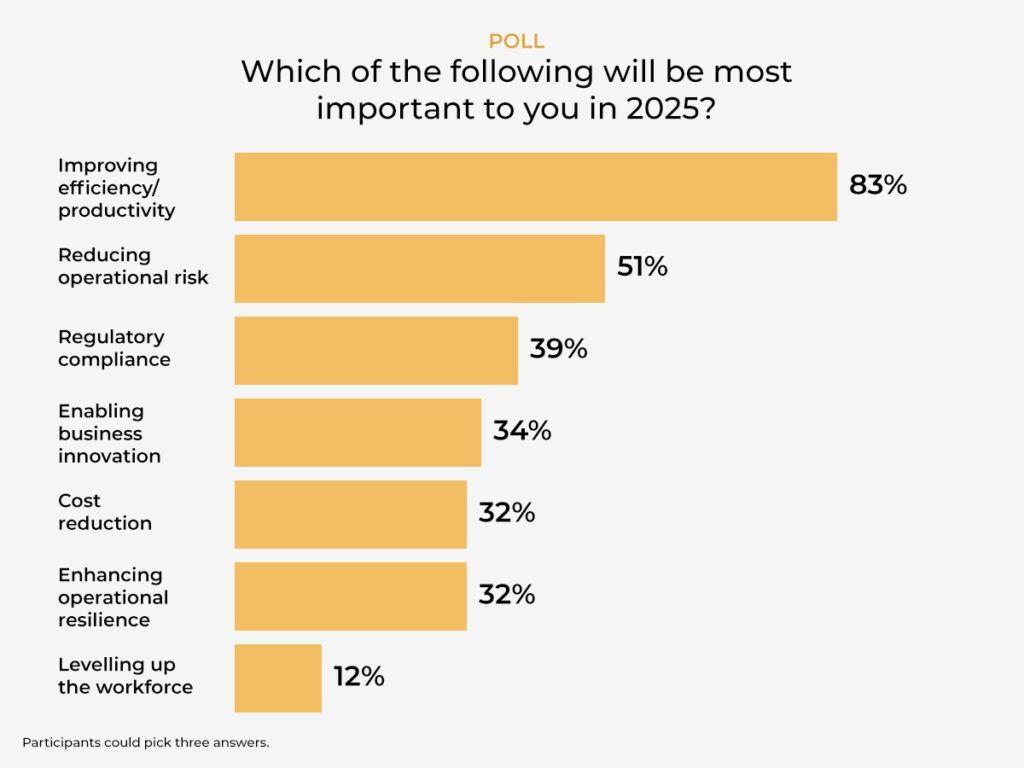

And how does that compare to the feeling in the room? We asked our audience to pick three top priorities in the coming year. Improving efficiency and productivity was the most common, making it into the top three for 83% of our audience.

Efficiency is clearly going to be a key driver for Operations teams in 2025.

When we talk about transformation, we often think about leaders driving that process. But their own roles are undergoing change as well. Mia explained that there was a growing feeling among many of the COOs interviewed that their role was evolving and they were being invited to contribute to business-wide strategic decisions.

Underpinning a lot of the headline goals, whether evolving the operating model, reducing costs or becoming more data-driven, was the topic of inefficient processes. The panel discussed how difficult it is to change processes in large financial firms, due to their complexity, their siloed nature and the number of legacy systems.

This explains why 73% of COOs interviewed by AFME felt that process transformation was going to be the most impactful strategy for 2025. Our panellists in the room agreed, noting that new technology often isn’t as transformational as it could be because firms don’t look at evolving the processes around it.

Future of Ops: The path to a next-gen operating model

Left to right: Danielle Price (Duco), Leon Clarke (MUFG Securities), Daniel Wright (HSBC) and Emma Prophet (TP ICAP)

Next generation operating models came up a few times during the other sessions, so it was only fitting that the Innovation Day agenda ended with a panel on just that topic.

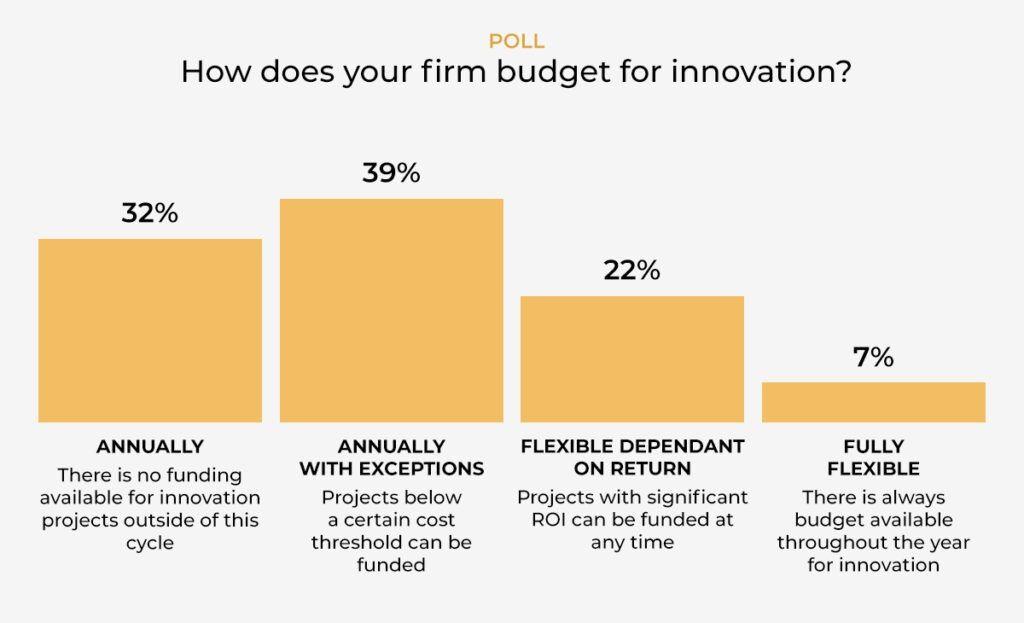

But before we got down to what innovation was needed, we wanted to find out from our audience how they were likely to fund it. Our poll revealed that most firms are still on an annual budget cycle when it comes to innovation, although the majority had some wiggle room for low-cost projects.

Duco’s Chief Financial Officer Danielle Price led the discussion with:

- Leon Clarke, Managing Director: Head of EMEA Markets Operations at MUFG

- Daniel Wright, MD, Head of Strategy & Change Delivery, Markets & Securities Services Operations at HSBC

- Emma Prophet, Group Head of Operations at TP ICAP

The discussion started by returning to a big topic from the previous panel: employee experience.

The discussion covered a lot of ground, including the way that Operations is now being given more control over the technology they use and their overall strategy. In particular, it’s innovations such as low and no-code technology that are empowering staff and enabling the kind of purpose-driven work that today’s workforce is looking for.

Our panellists also explored how the operating model of the future relies on removing boundaries between functions. Instead of technologists providing solutions, the industry has moved towards technologists facilitating business processes. This has brought Operations leaders closer to their technology teams.

Everyone should be encouraged to think bigger and truly explore the potential of new technology – as long as the appropriate guardrails are in place. As was observed in the COO panel, there’s a tendency for new technology to be underutilised otherwise.

One of the key aspects of an operating model of the future that emerged is that it needs to be futureproof. The industry changes a lot in the space of a few years. It’s important when considering technology change to think not just about the value the contract delivers today in terms of price, but how the technology will continue to generate ROI over several years.

Key takeaways from Innovation Day

The sessions covered a lot of different topics, with a diverse group of speakers from all across technology and capital markets. Some key themes returned again and again, though.

Employee experience and the workforce of the future

It’s clear that as well as being inefficient, expensive and risky, low-value manual work is a blocker to attracting talent. Whether we’re talking about automating low-value manual work or how users interact with the latest technology, the experience is vital to drive full adoption and success.

Evolving roles

COOs are finding they have a wider remit and are involved in strategic decisions. This in turn means they’re expecting more of their Heads of Operations. Upskilling is important at all levels.

AI is powerful, but easy (and expensive) to get wrong

There’s more education needed, but also the need to focus on using the right tool for the job. AI is very successful where the scope is well-defined. But it is costly and time-consuming when it fails. And AI projects currently fail most of the time.

Efficiency is on everyone’s agenda, from Operations leaders to investors

Next year banks are forecast to have the breathing room to tackle the structural drivers of cost and complexity – and are expected to do so.

We’ll be bringing you detailed coverage of each of the panel sessions over the coming weeks, so keep an eye out for even more insights. Follow us on LinkedIn and subscribe to our newsletter to ensure you don’t miss an update!